8 Linear regression models

8.1 Introduction

This chapter continues the theme of analysing statistical associations between variables. The methods described here are appropriate when the response variable \(Y\) is a continuous, interval level variable. We will begin by considering bivariate situations where the only explanatory variable \(X\) is also a continuous variable. Section 8.2 first discusses graphical and numerical descriptive techniques for this case, focusing on two very commonly used tools: a scatterplot of two variables, and a measure of association known as the correlation coefficient. Section 8.3 then describes methods of statistical inference for associations between two continuous variables. This is done in the context of a statistical model known as the simple linear regression model.

The ideas of simple linear regression modelling can be extended to a much more general and powerful set methods known as multiple linear regression models. These can have several explanatory variables, which makes it possible to examine associations between any explanatory variable and the response variable, while controlling for other explanatory variables. An important reason for the usefulness of these models is that they play a key role in statistical analyses which correspond to research questions that are causal in nature. As an interlude, we discuss issues of causality in research design and analysis briefly in Section 8.4. Multiple linear models are then introduced in Section 8.5. The models can also include categorical explanatory variables with any number of categories, as explained in Section 8.6.

The following example will be used for illustration throughout this chapter:

Example 8.1: Indicators of Global Civil Society

The Global Civil Society 2004/5 yearbook gives tables of a range of characteristics of the countries of the world.39 The following measures will be considered in this chapter:

Gross Domestic Product (GDP) per capita in 2001 (in current international dollars, adjusted for purchasing power parity)

Income level of the country in three groups used by the Yearbook, as Low income, Middle income or High income

Income inequality measured by the Gini index (with 0 representing perfect equality and 100 perfect inequality)

A measure of political rights and civil liberties in 2004, obtained as the average of two indices for these characteristics produced by the Freedom House organisation (1 to 7, with higher values indicating more rights and liberties)

World Bank Institute’s measure of control of corruption for 2002 (with high values indicating low levels of corruption)

Net primary school enrolment ratio 2000-01 (%)

Infant mortality rate 2001 (% of live births)

We will discuss various associations between these variables. It should be noted that the analyses are mainly illustrative examples, and the choices of explanatory and response variables do not imply any strong claims about causal connections between them. Also, the fact that different measures refer to slightly different years is ignored; in effect, we treat each variable as a measure of “recent” situation in the countries. The full data set used here includes 165 countries. Many of the variables are not available for all of them, so most of the analyses below use a smaller number of countries.

8.2 Describing association between two continuous variables

8.2.1 Introduction

Suppose for now that we are considering data on two continuous variables. The descriptive techniques discussed in this section do not strictly speaking require a distinction between an explanatory variable and a response variable, but it is nevertheless useful in many if not most applications. We will reflect this in the notation by denoting the variables \(X\) (for the explanatory variable) and \(Y\) (for the response variable). The observed data consist of the pairs of observations \((X_{1}, Y_{1}), (X_{2}, Y_{2}), \dots, (X_{n}, Y_{n})\) of \(X\) and \(Y\) for each of the \(n\) subjects in a sample, or, with more concise notation, \((X_{i}, Y_{i})\) for \(i=1,2,\dots,n\).

We are interested in analysing the association between \(X\) and \(Y\). Methods for describing this association in the sample are first described in this section, initially with some standard graphical methods in Section 8.2.2. This leads to a discussion in Section 8.2.3 of what we actually mean by associations in this context, and then to a definion of numerical summary measures for such associations in Section 8.2.4. Statistical inference for the associations will be considered in Section 8.3.

8.2.2 Graphical methods

Scatterplots

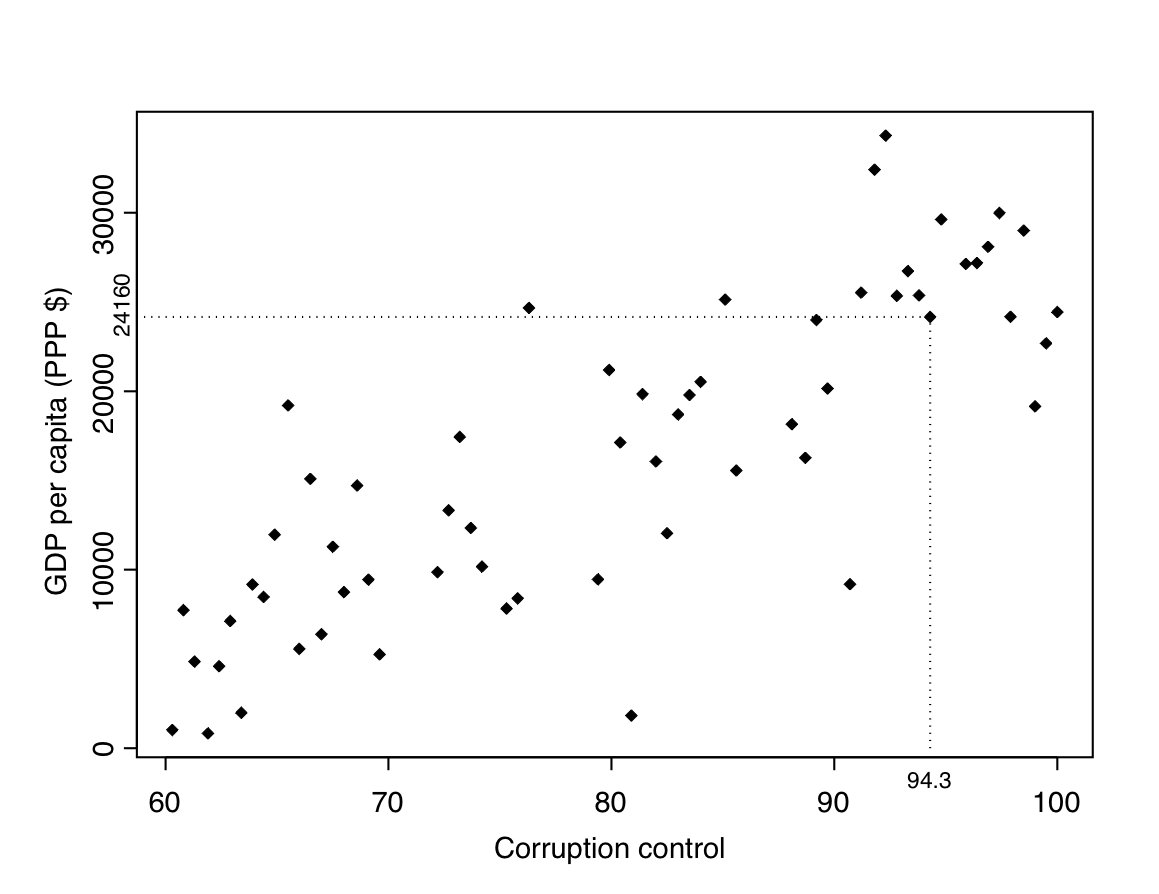

The standard statistical graphic for summarising the association between two continuous variables is a scatterplot. An example of it is given in Figure 8.1, which shows a scatterplot of Control of corruption against GDP per capita for 61 countries for which the corruption variable is at least 60 (the motivation of this restriction will be discussed later). The two axes of the plot show possible values of the two variables. The horizontal axis, here corresponding to Control of corruption, is conventionally used for the explanatory variable \(X\), and is often referred to as the X-axis. The vertical axis, here used for GDP per capita, then corresponds to the response variable \(Y\), and is known as the Y-axis.

The observed data are shown as points in the scatterplot, one for each of the \(n\) units. The location of each point is determined by its values of \(X\) and \(Y\). For example, Figure 8.1 highlights the observation for the United Kingdom, for which the corruption measure (\(X\)) is 94.3 and GDP per capita (\(Y\)) is $24160. The point for UK is thus placed at the intersection of a vertical line drawn from 94.3 on the \(X\)-axis and a horizontal line from 24160 on the \(Y\)-axis, as shown in the plot.

The principles of good graphical presentation on clear labelling, avoidance of spurious decoration and so on (c.f. Section 2.8) are the same for scatterplots as for any statistical graphics. Because the crucial visual information in a scatterplot is the shape of the cloud of the points, it is now often not necessary for the scales of the axes to begin at zero, especially if this is well outside the ranges of the observed values of the variables (as it is for the \(X\)-axis of Figure 8.1). Instead, the scales are typically selected so that the points cover most of the plotting surface. This is done by statistical software, but there are many situations were it is advisable to overrule the automatic selection (e.g. for making scatterplots of the same variables in two different samples directly comparable).

The main purpose of a scatterplot is to examine possible associations between \(X\) and \(Y\). Loosely speaking, this means considering the shape and orientation of the cloud of points in the graph. In Figure 8.1, for example, it seems that most of the points are in a cluster sloping from lower left to upper right. This indicates that countries with low levels of Control of corruption (i.e. high levels of corruption itself) tend to have low GDP per capita, and those with little corruption tend to have high levels of GDP. A more careful discussion of such associations again relates them to the formal definition in terms of conditional distributions, and also provides a basis for the methods of inference introduced later in this chapter. We will resume the discussion of these issues in Section 8.2.3 below. Before that, however, we will digress briefly from the main thrust of this chapter in order to describe a slightly different kind of scatterplot.

Line plots for time series

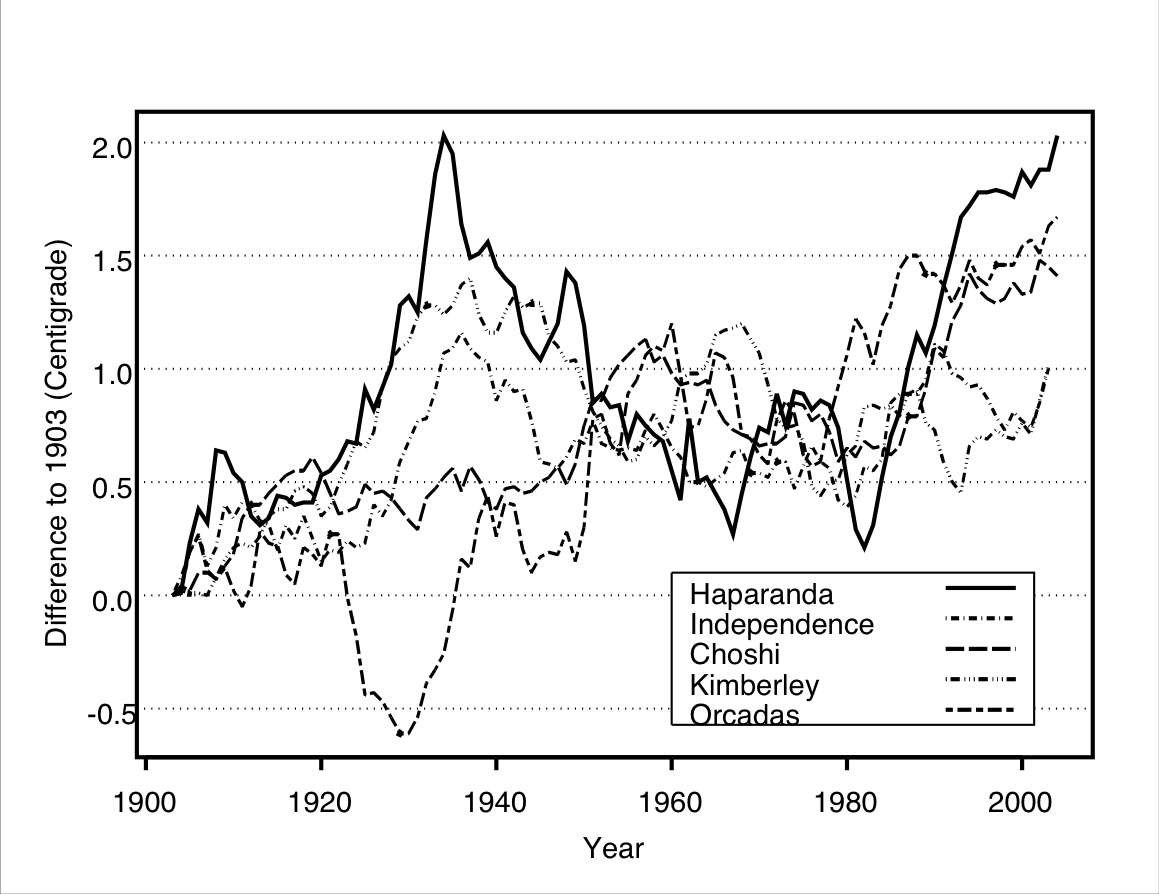

A very common special case of a scatterplot is one where the observations correspond to measurements of a variable for the same unit at several occasions over time. This is illustrated by the following example (another one is Figure 2.9):

Example: Changes in temperature, 1903–2004

Figure 8.2 summarises data on average annual temperatures over the past century in five locations. The data were obtained from the GISS Surface Temperature (GISTEMP) database maintained by the NASA Goddard Institute for Space Studies.40 The database contains time series of average monthly surface temperatures from several hundred meterological stations across the world. The five sites considered here are Haparanda in Northern Sweden, Independence, Kansas in the USA, Choshi on the east coast of Japan, Kimberley in South Africa, and the Base Orcadas Station on Laurie Island, off the coast of Antarctica. These were chosen rather haphazardly for this illustration, with the aim of obtaining a geographically scattered set of rural or small urban locations (to avoid issues with the heating effects of large urban areas). The temperature for each year at each location is here recorded as the difference from the temperature at that location in 1903.41

Consider first the data for Haparanda only. Here we have two variables, year and temperature, and 102 pairs of observations of them, one for each year between 1903 and 2004. These pairs could now be plotted in a scatterplot as described above. Here, however, we can go further to enhance the visual effect of the plot. This is because the observations represent measurements of a variable (temperature difference) for the same unit (the town of Haparanda) at several successive times (years). These 102 measurements form a time series of temperature differences for Haparanda over 1903–2004. A standard graphical trick for such series is to connect the points for successive times by lines, making it easy for the eye to follow the changes over time in the variable on the \(Y\)-axis. In Figure 8.2 this is done for Haparanda using a solid line. Note that doing this would make no sense for scatter plots like the one in Figure 8.1, because all the points there represent different subjects, in that case countries.

We can easily include several such series in the same graph. In Figure 8.2 this is done by plotting the temperature differences for each of the five locations using different line styles. The graph now summarises data on three variables, year, temperature and location. We can then examine changes over time for any one location, but also compare patterns of changes between them. Here there is clearly much variation within and between locations, but also some common features. Most importantly, the temperatures have all increased over the past century. In all five locations the average annual temperatures at the end of the period were around 1–2\(^{\circ}\)C higher than in 1903.

A set of time series like this is an example of dependent data in the sense discussed in Section 7.5. There we considered cases with pairs of observations, where the two observations in each pair had to be treated as statistically dependent. Here all of the temperature measurements for one location are dependent, probably with strongest dependence between adjacent years and less dependence between ones further apart. This means that we will not be able to analyse these data with the methods described later in this chapter, because these assume statistically independent observations. Methods of statistical modelling and inference for dependent data of the kind illustrated by the temperature example are beyond the scope of this course. This, however, does not prevent us from using a plot like Figure 8.2 to describe such data.

8.2.3 Linear associations

Consider again statistically independent observations of \((X_{i}, Y_{i})\), such as those displayed in Figure 8.1. Recall the definition that two variables are associated if the conditional distribution of \(Y\) given \(X\) is different for different values of \(X\). In the two-sample examples of Chapter 7 this could be examined by comparing two conditional distributions, since \(X\) had only two possible values. Now, however, \(X\) has many (in principle, infinitely many) possible values, so we will need to somehow define and compare conditional distributions given each of them. We will begin with a rather informal discussion of how this might be done. This will lead directly to a more precise and formal definition introduced in Section 8.3.

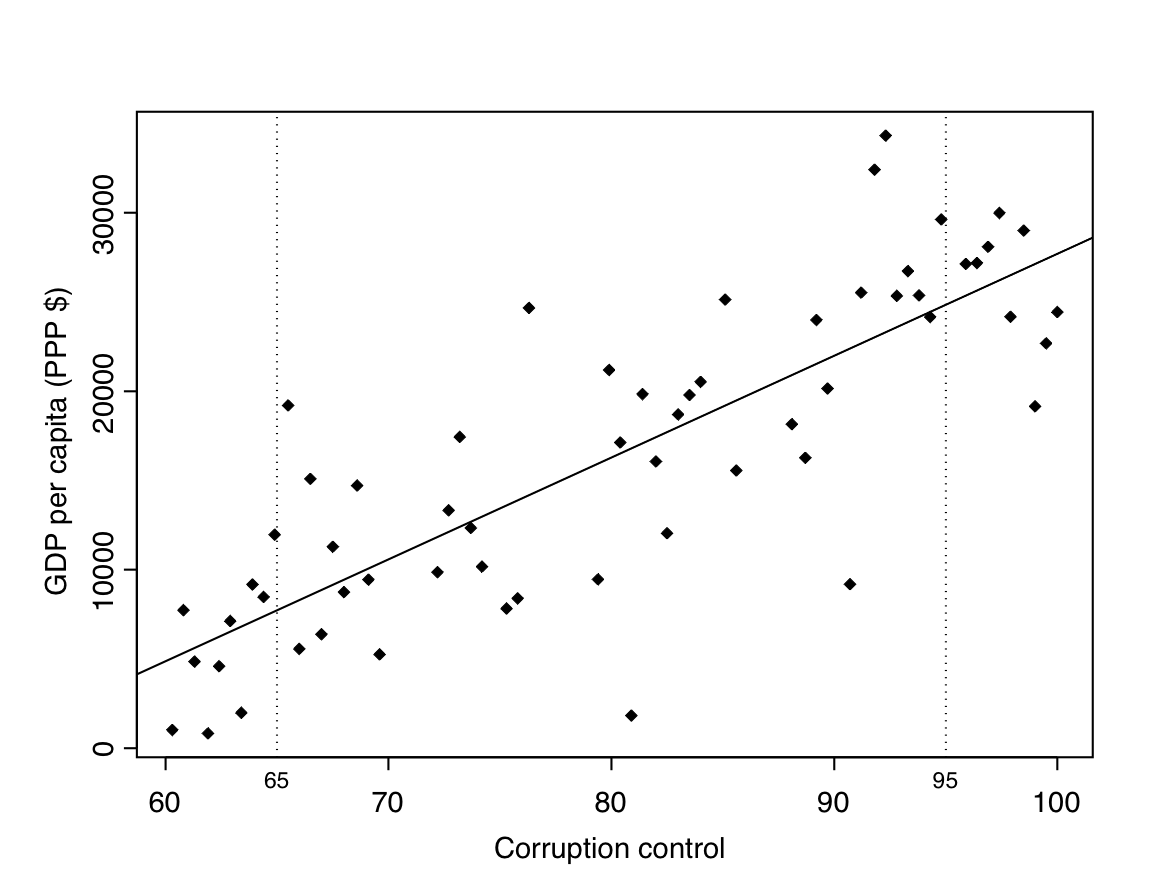

Figure 8.3 shows the same scatterplot as Figure 8.1. Consider first one value of \(X\) (Control of corruption), say 65. To get a rough idea of the conditional distribution of \(Y\) (GDP per capita) given this value of \(X\), we could examine the sample distribution of the values of \(Y\) for the units for which the value of \(X\) is close to 65. These correspond to the points near the vertical line drawn at \(X=65\) in Figure 8.3. This can be repeated for any value of \(X\); for example, Figure 8.3 also includes a vertical reference line at \(X=95\), for examining the conditional distribution of \(Y\) given \(X=95\).42

As in Chapter 7, associations between variables will here be considered almost solely in terms of differences in the means of the conditional distributions of \(Y\) at different values of \(X\). For example, Figure 8.3 suggests that the conditional mean of \(Y\) when X is 65 is around or just under 10000. At \(X=95\), on the other hand, the conditional mean seems to be between 20000 and 25000. The mean of \(Y\) is thus higher at the larger value of X. More generally, this finding is consistent across the scatterplot, in that the conditional mean of \(Y\) appears to increase when we consider increasingly large values of \(X\), indicating that higher levels of Control of corruption are associated with higher average levels of GDP. This is often expressed by saying that the conditional mean of \(Y\) increases when we “increase” \(X\).43 This is the sense in which we will examine associations between continuous variables: does the conditional mean of \(Y\) change (increase or decrease) when we increase \(X\)? If it does, the two variables are associated; if it does not, there is no association of this kind. This definition also agrees with the one linking association with prediction: if the mean of \(Y\) is different for different values of \(X\), knowing the value of \(X\) will clearly help us in making predictions about likely values of \(Y\). Based on the information in Figure 8.3, for example, our best guesses of the GDPs of two countries would clearly be different if we were told that the control of corruption measure was 65 for one country and 95 for the other.

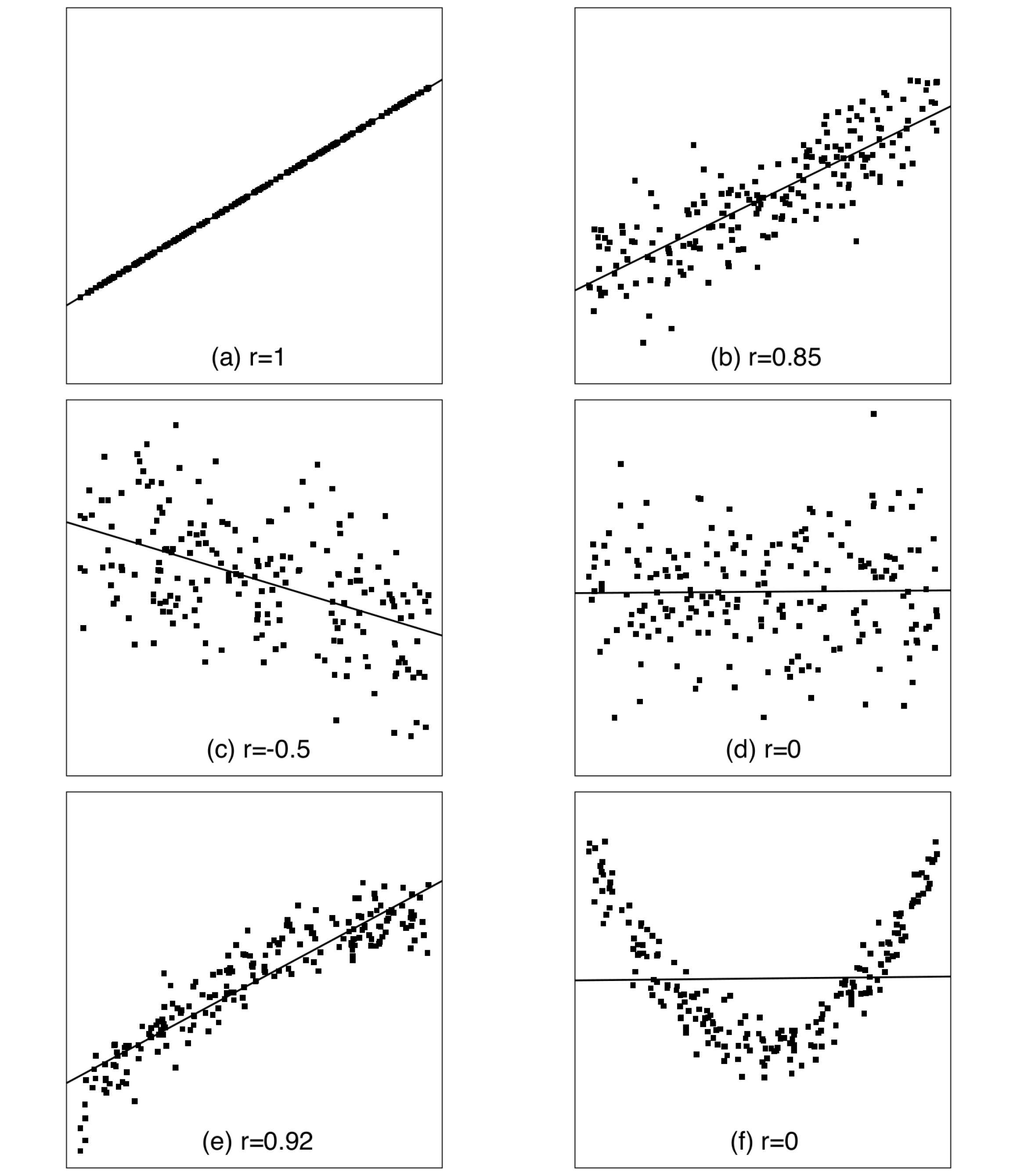

The nature of the association between \(X\) and \(Y\) is characterised by how the values of \(Y\) change when \(X\) increases. First, it is almost always reasonable to conceive these changes as reasonably smooth and gradual. In other words, if two values of \(X\) are close to each other, the conditional means of \(Y\) will be similar too; for example, if the mean of \(Y\) is 5 when \(X=10\), its mean when \(X=10.01\) is likely to be quite close to 5 rather than, say, 405. In technical terms, this means that the conditional mean of \(Y\) will be described by a smooth mathematical function of \(X\). Graphically, the means of \(Y\) as \(X\) increases will then trace a smooth curve in the scatterplot. The simplest possibility for such a curve is a straight line. This possibility is illustrated by plot (a) of Figure 8.4 (this and the other five plots in the figure display artificial data, generated for this illustration). Here all of the points fall on a line, so that when \(X\) increases, the values of \(Y\) increase at a constant rate. A relationship like this is known as a linear association between \(X\) and \(Y\). Linear associations are the starting point for examining associations between continuous variables, and often the only ones considered. In this chapter we too will focus almost completely on them.

In plot (a) of Figure 8.4 all the points are exactly on the straight line. This indicates a perfect linear association, where \(Y\) can be predicted exactly if \(X\) is known, so that the association is deterministic. Such a situation is neither realistic in practice, nor necessary for the association to be described as linear. All that is required for the latter is that the conditional means of \(Y\) given different values of \(X\) fall (approximately) on a straight line. This is illustrated by plot (b) of Figure 8.4, which shows a scatterplot of individual observations together with an approximation of the line of the means of \(Y\) given \(X\) (how the line was drawn will be explained later). Here the linear association is not perfect, as the individual points are not all on the same line but scattered around it. Nevertheless, the line seems to capture an important systematic feature of the data, which is that the average values of \(Y\) increase at an approximately constant rate as \(X\) increases. This combination of systematic and random elements is characteristic of all statistical associations, and it is also central to the formal setting for statistical inference for linear associations described in Section 8.3 below.

The direction of a linear association can be either positive or negative. Plots (a) and (b) of Figure 8.4 show a positive association, because increasing \(X\) is associated with increasing average values of \(Y\). This is indicated by the upward slope of the line describing the association. Plot (c) shows an example of a negative association, where the line slopes downwards and increasing values of \(X\) are associated with decreasing values of \(Y\). The third possibility, illustrated by plot (d), is that the line slopes neither up nor down, so that the mean of \(Y\) is the same for all values of \(X\). In this case there is no (linear) association between the variables.

Not all associations between continuous variables are linear, as shown by the remaining two plots of Figure 8.4. These illustrate two kinds of nonlinear associations. In plot (e), the association is still clearly monotonic, meaning that average values of \(Y\) change in the same direction — here increase — when \(X\) increases. The rate of this increase, however, is not constant, as indicated by the slightly curved shape of the cloud of points. The values of \(Y\) seem to increase faster for small values of \(X\) than for large ones. A straight line drawn through the scatterplot captures the general direction of the increase, but misses its nonlinearity. One practical example of such a relationship is the one between years of job experience and salary: it is often found that salary increases fastest early on in a person’s career and more slowly later on.

Plot (f) shows a nonlinear and nonmonotonic relationship: as \(X\) increases, average values of \(Y\) first decrease to a minimum, and then increase again, resulting in a U-shaped scatterplot. A straight line is clearly an entirely inadequate description of such a relationship. A nonmonotonic association of this kind might be seen, for example, when considering the dependence of the failure rates of some electrical components (\(Y\)) on their age (\(X\)). It might then be that the failure rates were high early (from quick failures of flawed components) and late on (from inevitable wear and tear) and lowest in between for “middle-aged but healthy” components.

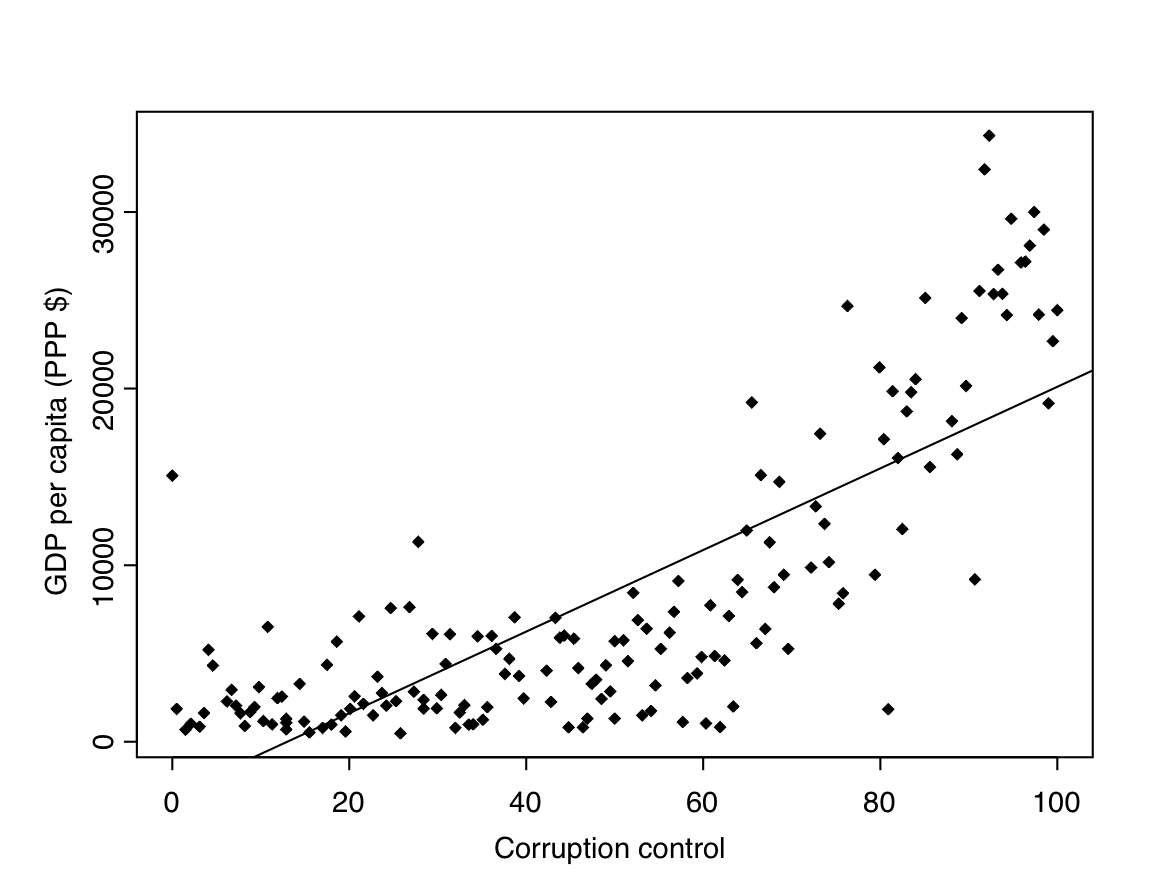

Returning to real data, recall that we have so far considered control of corruption and GDP per capita only among countries with a Control of corruption score of at least 60. The scatterplot for these, shown in Figure 8.3, also includes a best-fitting straight line. The observed relationship is clearly positive, and seems to be fairly well described by a straight line. For countries with relatively low levels of corruption, the association between control of corruption and GDP can be reasonably well characterised as linear.

Consider now the set of all countries, including also those with high levels of corruption (scores of less than 60). In a scatterplot for them, shown in Figure 8.5, the points with at least 60 on the \(X\)-axis are the same as those in Figure 8.3, and the new points are to the left of them. The plot now shows a nonlinear relationship comparable to the one in plot (e) of Figure 8.4. The linear relationship which was a good description for the countries considered above is thus not adequate for the full set of countries. Instead, it seems that the association is much weaker for the countries with high levels of corruption, essentially all of which have fairly low values of GDP per capita. The straight line fitted to the plot identifies the overall positive association, but cannot describe its nonlinearity. This example further illustrates how scatterplots can be used to examine relationships between variables and to assess whether they can be best described as linear or nonlinear associations.44

So far we have said nothing about how the exact location and direction of the straight lines shown in the figures have been selected. These are determined so that the fitted line is in a certain sense the best possible one for describing the data in the scatterplot. Because the calculations needed for this are also (and more importantly) used in the context of statistical inference for such data, we will postpone a description of them until Section 8.3.4. For now we can treat the line simply as a visual summary of the linear association in a scatterplot.

8.2.4 Measures of association: covariance and correlation

A scatterplot is a very powerful tool for examining sample associations of pairs of variables in detail. Sometimes, however, this is more than we really need for an initial summary of a data set, especially if there are many variables and thus many possible pairs of them. It is then convenient also to be able to summarise each pairwise association using a single-number measure of association. This section introduces the correlation coefficient, the most common such measure for continuous variables. It is a measure of the strength of linear associations of the kind defined above.

Suppose that we consider two variables, denoted \(X\) and \(Y\). This again implies a distinction between an explanatory and a response variable, to maintain continuity of notation between different parts of this chapter. The correlation coefficient itself, however, is completely symmetric, so that its value for a pair of variables will be the same whether or not we treat one or the other of them as explanatory for the other. First, recall from equation of standard deviation towards the end of Section 2.6.2 that the sample standard deviations of the two variables are calculated as \[\begin{equation} s_{x} = \sqrt{\frac{\sum(X_{i}-\bar{X})^{2}}{n-1}} \text{and} s_{y} = \sqrt{\frac{\sum (Y_{i}-\bar{Y})^{2}}{n-1}} \tag{8.1} \end{equation}\] where the subscripts \(x\) and \(y\) identify the two variables, and \(\bar{X}\) and \(\bar{Y}\) are their sample means. A new statistic is the sample covariance between \(X\) and \(Y\), defined as \[\begin{equation} s_{xy} = \frac{\sum (X_{i}-\bar{X})(Y_{i}-\bar{Y})}{n-1}. \tag{8.2} \end{equation}\] This is a measure of linear association between \(X\) and \(Y\). It is positive if the sample association is positive and negative if the association is negative.

In theoretical statistics, covariance is the fundamental summary of sample and population associations between two continuous variables. For descriptive purposes, however, it has the inconvenient feature that its magnitude depends on the units in which \(X\) and \(Y\) are measured. This makes it difficult to judge whether a value of the covariance for particular variables should be regarded as large or small. To remove this complication, we can standardise the sample covariance by dividing it by the standard deviations, to obtain the statistic \[\begin{equation} r=\frac{s_{xy}}{s_{x}s_{y}} = \frac{\sum (X_{i}-\bar{X})(Y_{i}-\bar{Y})}{\sqrt{\sum\left(X_{i}-\bar{X}\right)^{2} \sum\left(Y_{i}-\bar{Y}\right)^{2}}}. \tag{8.3} \end{equation}\] This is the (sample) correlation coefficient, or correlation for short, between \(X\) and \(Y\). It is also often (e.g. in SPSS) known as Pearson’s correlation coefficient after Karl Pearson (of the \(\chi^{2}\) test, see first footnote in Chapter 4), although both the word and the statistic are really due to Sir Francis Galton.45

The properties of the correlation coefficient can be described by going through the same list as for the \(\gamma\) coefficient in Section 2.4.5. While doing so, it is useful to refer to the examples in Figure 8.4, where the correlations are also shown.

Sign: Correlation is positive if the linear association between the variables is positive, i.e. if the best-fitting straight line slopes upwards (as in plots a, b and e) and negative if the association is negative (c). A zero correlation indicates complete lack of linear association (d and f).

Extreme values: The largest possible correlation is \(+1\) (plot a) and the smallest \(-1\), indicating perfect positive and negative linear associations respectively. More generally, the magnitude of the correlation indicates the strength of the association, so that the closer to \(+1\) or \(-1\) the correlation is, the stronger the association (e.g. compare plots a–d). It should again be noted that the correlation captures only the linear aspect of the association, as illustrated by the two nonlinear cases in Figure 8.4. In plot (e), there is curvature but also a strong positive trend, and the latter is reflected in a fairly high correlation. In plot (f), the trend is absent and the correlation is 0, even though there is an obvious nonlinear relationship. Thus the correlation coefficient is a reasonable initial summary of the strength of association in (e), but completely misleading in (f).

Formal interpretation: The correlation coefficient cannot be interpreted as a Proportional Reduction in Error (PRE) measure, but its square can. The latter statistic, so-called coefficient of determination or \(R^{2}\), is described in Section 8.3.3.

Substantive interpretation: As with any measure of association, the question of whether a particular sample correlation is high or low is not a purely statistical question, but depends on the nature of the variables. This can be judged properly only with the help of experience of correlations between similar variables in different contexts. As one very rough rule thumb it might be said that in many social science contexts correlations greater than 0.4 (or smaller than \(-0.4\)) would typically be considered noteworthy and ones greater than 0.7 quite strong.

Returning to real data, Table 8.1 shows the correlation coefficients for all fifteen distinct pairs of the six continuous variables in the Global Civil Society data set mentioned in Example 8.1. This is an example of a correlation matrix, which is simply a table with the variables as both its rows and columns, and the correlation between each pair of variables given at the intersection of corresponding row and column. For example, the correlation of GDP per capita and School enrolment is here 0.42. This is shown at the intersection of the first row (GDP) and fifth column (School enrolment), and also of the fifth row and first column. In general, every correlation is shown twice in the matrix, once in its upper triangle and once in the lower. The triangles are separated by a list of ones on the diagonal of the matrix. This simply indicates that the correlation of any variable with itself is 1, which is true by definition and thus of no real interest.

| Variable | GDP | Gini | Pol. | Corrupt. | School | IMR |

|---|---|---|---|---|---|---|

| GDP per capita [GDP ] | 1 | -0.39 | 0.51 | 0.77 | 0.42 | -0.62 |

| Income inequality [Gini ] | -0.39 | 1 | -0.15 | -0.27 | -0.27 | 0.42 |

| Political rights [Pol. ] | 0.51 | -0.15 | 1 | 0.59 | 0.40 | -0.44 |

| Control of corruption [Corrupt. ] | 0.77 | -0.27 | 0.59 | 1 | 0.41 | -0.64 |

| School enrolment [School ] | 0.42 | -0.27 | 0.40 | 0.41 | 1 | -0.73 |

| Infant mortality [IMR ] | -0.62 | 0.42 | -0.44 | -0.64 | -0.73 | 1 |

All of the observed associations in this example are in unsurprising directions. For example, School enrolment is positively correlated with GDP, Political rights and Control of corruption, and negatively correlated with Income inequality and Infant mortality. In other words, countries with large percentages of children enrolled in primary school tend to have high levels of GDP per capita and of political rights and civil liberties, and low levels of corruption, income inequality and infant mortality. The strongest associations in these data are between GDP per capita and Control of corruption (\(r=0.77\)) and School enrolment and Infant mortality rate (\(r=-0.73\)), and the weakest between Income inequality on the one hand and Political rights, Control of corruption and School enrolment on the other (correlations of \(-0.15\), \(-0.27\) and \(-0.27\) respectively).

These correlations describe only the linear element of sample associations, but give no hint of any nonlinear ones. For example, the correlation of 0.77 between GDP and Control of corruption summarises the way the observations cluster around the straight line shown in Figure 8.5. The correlation is high because this increase in GDP as Control of corruption increases is quite strong, but it gives no indication of the nonlinearity of the association. A scatterplot is needed for revealing this feature of the data. The correlation for the restricted set of countries shown in Figure 8.3 is 0.82.

A correlation coefficient can also be defined for the joint population distribution of two variables. The sample correlation \(r\) can then be treated as an estimate of the population correlation, which is often denoted by \(\rho\) (the lower-case Greek “rho”). Statistical inference for the population correlation can also be derived. For example, SPSS automatically outputs significance tests for the null hypothesis that \(\rho\) is 0, i.e. that there is no linear association between \(X\) and \(Y\) in the population. Here, however, we will not discuss this, choosing to treat \(r\) purely as a descriptive sample statistic. The next section provides a different set of tools for inference on population associations.

8.3 Simple linear regression models

8.3.1 Introduction

The rest of this course is devoted to the method of linear regression modelling. Its purpose is the analysis of associations in cases where the response variable is a continuous, interval level variable, and the possibly several explanatory variables can be of any type. We begin in this section with simple linear regression, where there is only one explanatory variable. We will further assume that this is also continuous. The situation considered here is thus the same as in the previous section, but here the focus will be on statistical inference rather than description. Most of the main concepts of linear regression can be introduced in this context. Those that go beyond it are described in subsequent sections. Section 8.5 introduces multiple regression involving more than one explanatory variable. The use of categorical explanatory variables in such models is explained in Section 8.6. Finally, Section 8.7 gives a brief review of some further aspects of linear regression modelling which are not covered on this course.

Example: Predictors of Infant Mortality Rate

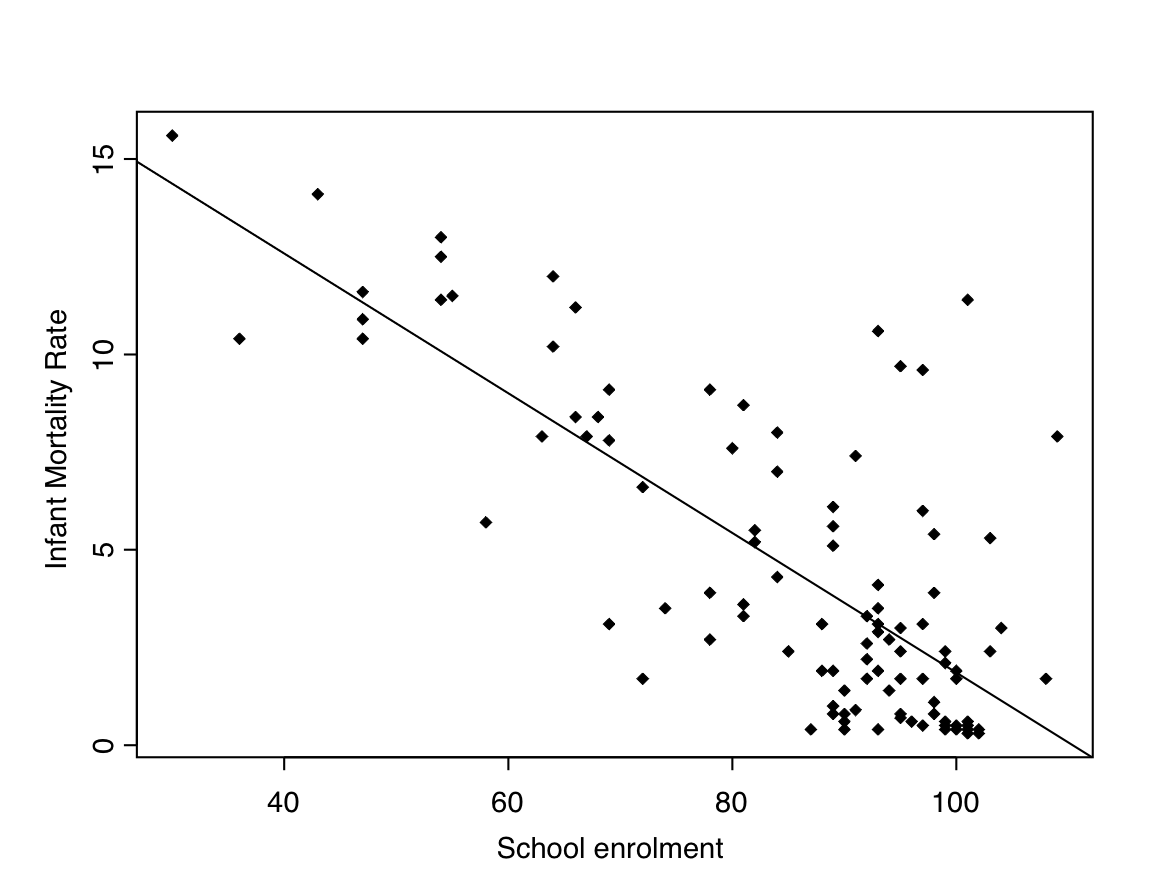

The concepts of linear regression models will be illustrated as they are introduced with a second example from the Global Civil Society data set. The response variable will now be Infant Mortality Rate (IMR). This is an illuminating outcome variable, because it is a sensitive and unquestionably important reflection of a country’s wellbeing; whatever we mean by “development”, it is difficult to disagree that high levels of it should coincide with low levels of infant mortality. We will initially consider only one explanatory variable, Net primary school enrolment ratio, referred to as “School enrolment” for short. This is defined as the percentage of all children of primary school age who are enrolled in school. Enrolment numbers and the population size are often obtained from different official sources, which sometimes leads to discrepancies. In particular, School enrolment for several countries is recorded as over 100, which is logically impossible. This is an illustration of the kinds of measurement errors often affecting variables in the social sciences. We will use the School enrolment values as recorded, even though they are known to contain some error.

A scatterplot of IMR vs. School enrolment is shown in Figure 8.6, together with the best-fitting straight line. Later we will also consider three additional explanatory variables: Control of corruption, Income inequality and Income level of the country in three categories (c.f. Example 8.1). For further reference, Table 8.2 shows various summary statistics for these variables. Throughout, the analyses are restricted to those 111 countries for which all of the five variables are recorded. For this reason the correlations in Table 8.2 differ slightly from those in Table 8.1, where each correlation was calculated for all the countries with non-missing values of that pair of variables.

|

IMR |

School enrolment | Control of corruption | Income inequality | |

|---|---|---|---|---|

| Summary statistics | ||||

| Mean | 4.3 | 86.1 | 50.1 | 40.5 |

| std. deviation | 4.0 | 16.7 | 28.4 | 10.2 |

| Minimum | 0.3 | 30.0 | 3.6 | 24.4 |

| Maximum | 15.6 | 109.0 | 100.0 | 70.7 |

| Correlation matrix | ||||

| IMR | 1 | -0.75 | -0.60 | 0.39 |

| School enrolment | -0.75 | 1 | 0.39 | -0.27 |

| Control of corruption | -0.60 | 0.39 | 1 | -0.27 |

| Income inequality | 0.39 | -0.27 | -0.27 | 1 |

| Means for countries in different income categories | ||||

| Low income (\(n=41\)) | 8.2 | 72.1 | 27.5 | 41.7 |

| Middle income (\(n=48\)) | 2.8 | 92.5 | 50.8 | 43.3 |

| High income (\(n=22\)) | 0.5 | 98.4 | 90.7 | 32.0 |

8.3.2 Definition of the model

The simple linear regression model defined in this section is a statistical model for a continuous, interval level response variable \(Y\) given a single explanatory variable \(X\), such as IMR given School enrolment. The model will be used to carry out statistical inference on the association between the variables in a population (which in the IMR example is clearly again of the conceptual variety).

For motivation, recall first the situation considered in Section 7.3. There the data consisted of observations \((Y_{i}, X_{i})\) for \(i=1,2,\dots,n\), which were assumed to be statistically independent. The response variable \(Y\) was continuous but \(X\) had only two possible values, coded 1 and 2. A model was then set up where the population distribution of \(Y\) had mean \(\mu_{1}\) and variance \(\sigma^{2}_{1}\) for units with \(X=1\), and mean \(\mu_{2}\) and variance \(\sigma^{2}_{2}\) when \(X=2\). In some cases it was further assumed that the population distributions were both normal, and that the population variances were equal, i.e. that \(\sigma^{2}_{1}=\sigma^{2}_{2}\), with their common value denoted \(\sigma^{2}\). With these further assumptions, which will also be used here, the model for \(Y\) given a dichotomous \(X\) stated that (1) observations for different units \(i\) were statistically independent; (2) each \(Y_{i}\) was sampled at random from a population distribution which was normal with mean \(\mu_{i}\) and variance \(\sigma^{2}\); and (3) \(\mu_{i}\) depended on \(X_{i}\) so that it was equal to \(\mu_{1}\) if \(X_{i}\) was 1 and \(\mu_{2}\) if \(X_{i}\) was 2.

The situation in this section is exactly the same, except that \(X\) is now continuous instead of dichotomous. We will use the same basic model, but will change the specification of the conditional mean \(\mu_{i}\) appropriately. In the light of the discussion in previous sections of this chapter, it is no surprise that this will be defined in such a way that it describes a linear association between \(X\) and \(Y\). This is done by setting \(\mu_{i}=\alpha+\beta X_{i}\), where \(\alpha\) and \(\beta\) are unknown population parameters. This is the equation of straight line (we will return to it in the next section). With this specification, the model for observations \((Y_{1},X_{1}), (Y_{2}, X_{2}), \dots, (Y_{n}, X_{n})\) becomes

Observations for different units \(i\) (\(=1,2,\dots,n\)) are statistically independent.

Each \(Y_{i}\) is normally distributed with mean \(\mu_{i}\) and variance \(\sigma^{2}\).

The means \(\mu_{i}\) depend on \(X_{i}\) through \(\mu_{i}=\alpha+\beta X_{i}\).

Often the model is expressed in an equivalent form where 2. and 3. are combined as \[\begin{equation} Y_{i}=\alpha+\beta X_{i} +\epsilon_{i} \tag{8.4} \end{equation}\] where each \(\epsilon_{i}\) is normally distributed with mean 0 and variance \(\sigma^{2}\). The \(\epsilon_{i}\) are known as error terms or population residuals (and the letter \(\epsilon\) is the lower-case Greek “epsilon”). This formulation of the model clearly separates the mean of \(Y_{i}\), which traces the straight line \(\alpha+\beta X_{i}\) as \(X_{i}\) changes, from the variation around that line, which is described by the variability of \(\epsilon_{i}\).

The model defined above is known as the simple linear regression model:

Simple because it has only one explanatory variable, as opposed to multiple linear regression models which will have more than one.

Linear because it specifies a linear association between \(X\) and \(Y\).46

Regression: This is now an established part of the name of the model, although the origins of the word are not central to the use of the model.47

-

Model, because this is a statistical model in the sense discussed in the middle of Section 6.3.1. In other words, the model is always only a simplified abstraction of the true, immeasurably complex processes which determine the values of \(Y\). Nevertheless, it is believed that a well-chosen model can be useful for explaining and predicting observed values of \(Y\). This spirit is captured by the well-known statement by the statistician George Box:48

All models are wrong, but some are useful.

A model like this has the advantage that it reduces the examination of associations in the population to estimation and inference on a small number of model parameters, in the case of the simple linear regression model just \(\alpha\), \(\beta\) and \(\sigma^{2}\).

Of course, not all models are equally appropriate for given data, and some will be both wrong and useless. The results from a model should thus be seriously presented and interpreted only if the model is deemed to be reasonably adequate. For the simple linear regression model, this can be partly done by examining whether the scatterplot between \(X\) and \(Y\) appears to be reasonably consistent with a linear relationship. Some further comments on the assessment of model adequacy will be given in Section 8.7.

8.3.3 Interpretation of the model parameters

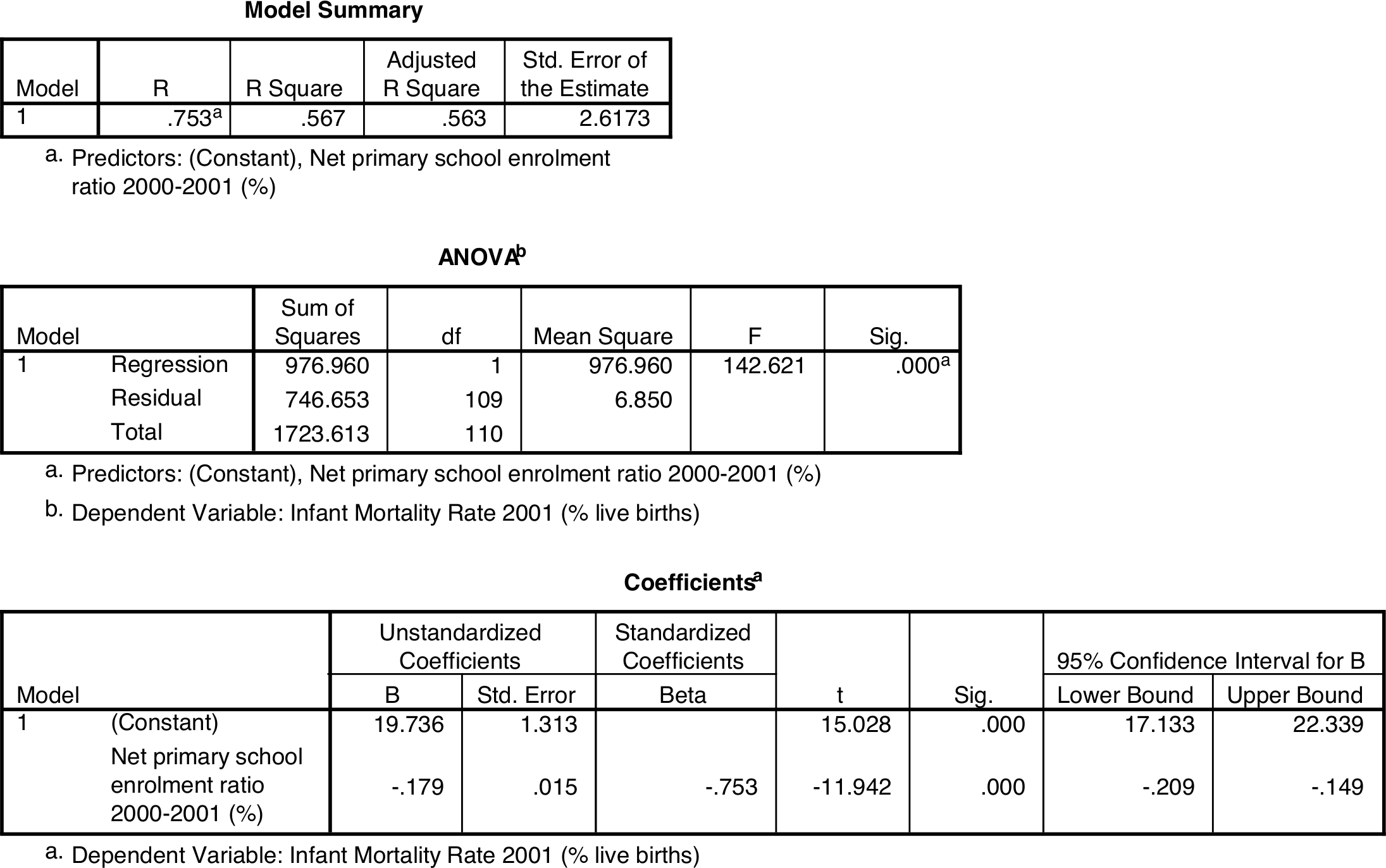

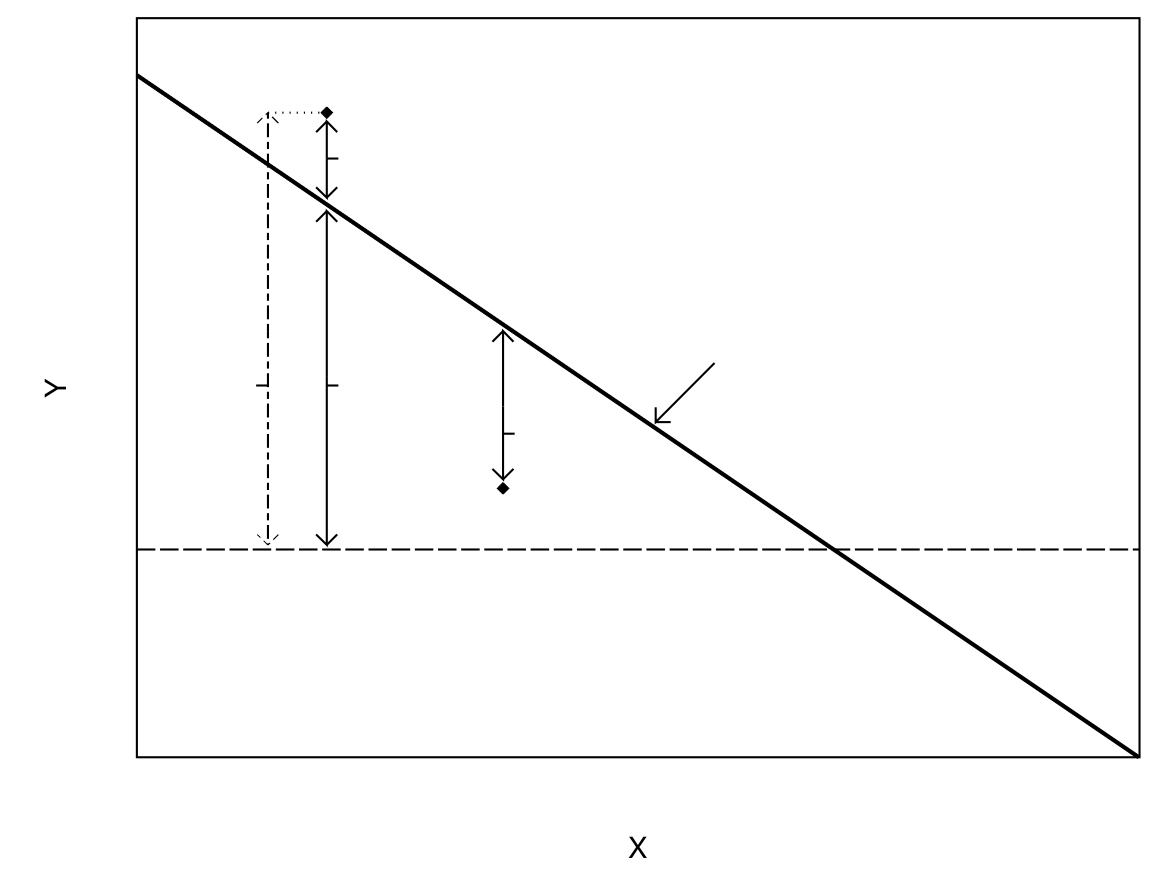

The simple linear regression model ((8.4)) has three parameters, \(\alpha\), \(\beta\) and \(\sigma^{2}\). Each of these has its own interpretation, which are explained in this section. Sometimes it will be useful to illustrate the definition with specific numerical values, for which we will use ones for the model for IMR given School enrolment in our example. SPSS output for this model is shown in Figure 8.7. Note that although these values are first used here to illustrate the interpretation of the population parameters in the model, they are of course only estimates (of a kind explained in the next section) of those parameters. Other parts of the SPSS output will be explained later in this chapter.

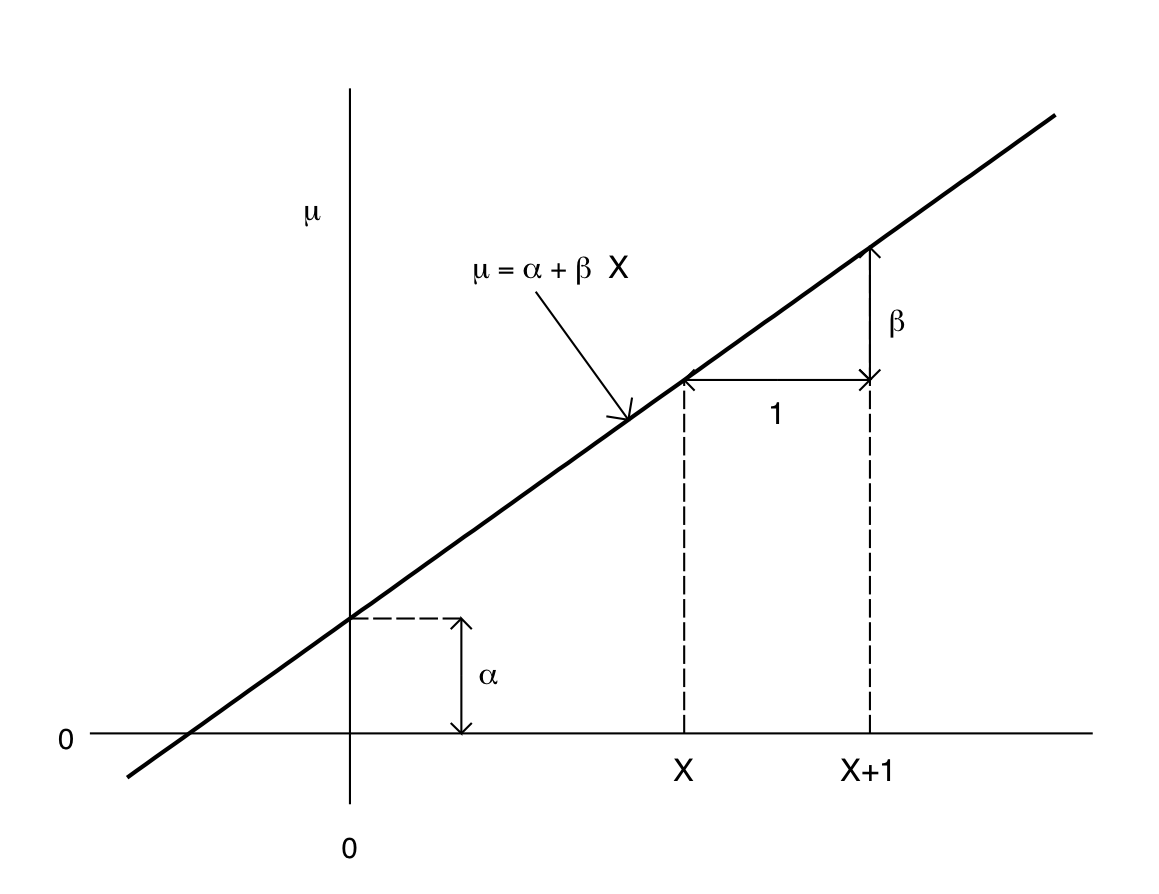

According to the model, the conditional mean (also often known as the conditional expected value) of \(Y\) given \(X\) in the population is (dropping the subscript \(i\) for now for notational simplicity) \(\mu=\alpha+\beta X\). The two parameters \(\alpha\) and \(\beta\) in this formula are known as regression coefficients. They are interpreted as follows:

\(\alpha\) is the expected value of \(Y\) when \(X\) is equal to 0. It is known as the intercept or constant term of the model.

\(\beta\) is the change in the expected value of \(Y\) when \(X\) increases by 1 unit. It is known as the slope term or the coefficient of \(X\).

Just to include one mathematical proof in this coursepack, these results can be derived as follows:

When \(X=0\), the mean of \(Y\) is \(\mu=\alpha+\beta X=\alpha+\beta\times 0 =\alpha+0=\alpha\).

-

Compare two observations, one with value \(X\) of the explanatory variable, and the other with one unit more, i.e. \(X+1\). The corresponding means of \(Y\) are

with \(X+1\): \(\mu\) \(=\alpha+\beta\times (X+1)\) \(=\alpha+\beta X +\beta\) with \(X\): \(\mu\) \(=\alpha+\beta X\) Difference: \(\beta\)

which completes the proof of the claims above — Q.E.D. In case you prefer a graphical summary, this is given in Figure 8.8.

The most important parameter of the model, and usually the only one really discussed in interpreting the results, is \(\beta\), the regression coefficient of \(X\). It is also called the slope because it is literally the slope of the regression line, as shown in Figure 8.8. It is the only parameter in the model which describes the association between \(X\) and \(Y\), and it does so in the above terms of expected changes in \(Y\) corresponding to changes in X (\(\beta\) is also related to the correlation between \(X\) and \(Y\), in a way explained in the next section). The sign of \(\beta\) indicates the direction of the association. When \(\beta\) is positive (greater than 0), the regression line slopes upwards and increasing \(X\) thus also increases the expected value of \(Y\) — in other words, the association between \(X\) and \(Y\) is positive. This is the case illustrated in Figure 8.8. If \(\beta\) is negative, the regression line slopes downwards and the association is also negative. Finally, if \(\beta\) is zero, the line is parallel with the \(X\)-axis, so that changing \(X\) does not change the expected value of \(Y\). Thus \(\beta=0\) corresponds to no (linear) association between \(X\) and \(Y\).

In the real example shown in Figure 8.7, \(X\) is School enrolment and \(Y\) is IMR. In SPSS output, the estimated regression coefficients are given in the “Coefficients” table in the column labelled “B” under “Unstandardized coefficients”. The estimated constant term \(\alpha\) is given in the row labelled “(Constant)”, and the slope term on the next row, labelled with the name or label of the explanatory variable as specified in the SPSS data file — here “Net primary school enrolment ratio 2000-2001 (%)”. The value of the intercept is here 19.736 and the slope coefficient is \(-0.179\). The estimated regression line for expected IMR is thus \(19.736-0.179 X\), where \(X\) denotes School enrolment. This is the line shown in Figure 8.6.

Because the slope coefficient in the example is negative, the association between the variables is also negative, i.e. higher levels of school enrolment are associated with lower levels of infant mortality. More specifically, every increase of one unit (here one percentage point) in School enrolment is associated with a decrease of 0.179 units (here percentage points) in expected IMR.

Since the meaning of \(\beta\) is related to a unit increase of the explanatory variable, the interpretation of its magnitude depends on what those units are. In many cases one unit of \(X\) is too small or too large for convenient interpretation. For example, a change of one percentage point in School enrolment is rather small, given that the range of this variable in our data is 79 percentage points (c.f. Table 8.2). In such cases the results can easily be reexpressed by using multiples of \(\beta\): specifically, the effect on expected value of \(Y\) of changing \(X\) by \(A\) units is obtained by multiplying \(\beta\) by \(A\). For instance, in our example the estimated effect of increasing School enrolment by 10 percentage points is to decrease expected IMR by \(10\times 0.179=1.79\) percentage points.

The constant term \(\alpha\) is a necessary part of the model, but it is almost never of interest in itself. This is because the expected value of \(Y\) at \(X=0\) is rarely specifically interesting. Very often \(X=0\) is also unrealistic, as in our example where it corresponds to a country with zero primary school enrolment. There are fortunately no such countries in the data, where the lowest School enrolment is 30%. It is then of no interest to discuss expected IMR for a hypothetical country where no children went to school. Doing so would also represent unwarranted extrapolation of the model beyond the range of the observed data. Even though the estimated linear model seems to fit reasonably well for these data, this is no guarantee that it would do so also for countries with much lower school enrolment, even if they existed.

The third parameter of the simple regression model is \(\sigma^{2}\). This is the variance of the conditional distribution of \(Y\) given \(X\). It is also known as the conditional variance of \(Y\), the error variance or the residual variance. Similarly, its square root \(\sigma\) is known as the conditional, error or residual standard deviation. To understand \(\sigma\), let us consider a single value of \(X\), such as one corresponding to one of the vertical dashed lines in Figure 8.8 or, say, school enrolment of 85 in Figure 8.6. The model specifies a distribution for \(Y\) given any such value of \(X\). If we were to (hypothetically) collect a large number of observations, all with this same value of \(X\), the distribution of \(Y\) for them would describe the conditional distribution of \(Y\) given that value of \(X\). The model states that the average of these values, i.e. the conditional mean of \(Y\), is \(\alpha+\beta X\), which is the point on the regression line corresponding to \(X\). The individual values of \(Y\), however, would of course not all be on the line but somewhere around it, some above and some below.

The linear regression model further specifies that the form of the conditional distribution of \(Y\) is approximately normal. You can try to visualise this by imagining a normal probability curve (c.f. Figure 6.5) on the vertical line from \(X\), centered on the regression line and sticking up from the page. The bell shape of the curve indicates that most of the values of \(Y\) for a given \(X\) will be close to the regression line, and only small proportions of them far from it. The residual standard deviation \(\sigma\) is the standard deviation of this conditional normal distribution, in essence describing how tightly concentrated values of \(Y\) tend to be around the regression line. The model assumes, mainly for simplicity, that the same value of \(\sigma\) applies to the conditional distributions at all values of \(X\); this is known as the assumption of homoscedasticity.

In SPSS output, an estimate of \(\sigma\) is given in the “Model Summary” table under the misleading label “Std. Error of the Estimate”. An estimate of the residual variance \(\sigma^{2}\) is found also in the “ANOVA” table under “Mean Square” for “Residual”. In our example the estimate of \(\sigma\) is 2.6173 (and that of \(\sigma^{2}\) is 6.85). This is usually not of direct interest for interpretation, but it will be a necessary component of some parts of the analysis discussed below.

8.3.4 Estimation of the parameters

Since the regression coefficients \(\alpha\) and \(\beta\) and the residual standard deviation \(\sigma\) are unknown population parameters, we will need to use the observed data to obtain sensible estimates for them. How to do so is now less obvious than in the cases of simple means and proportions considered before. This section explains the standard method of estimation for the parameters of linear regression models.

We will denote estimates of \(\alpha\) and \(\beta\) by \(\hat{\alpha}\) and \(\hat{\beta}\) (“alpha-hat” and “beta-hat”) respectively (other notations are also often used, e.g. \(a\) and \(b\)). Similarly, we can define \[\hat{Y}=\hat{\alpha}+\hat{\beta} X\] for \(Y\) given any value of \(X\). These are the values on the estimated regression line. They are known as fitted values for \(Y\), and estimating the parameters of the regression model is often referred to as “fitting the model” to the observed data. The fitted values represent our predictions of expected values of \(Y\) given \(X\), so they are also known as predicted values of \(Y\).

In particular, fitted values \(\hat{Y}_{i}=\hat{\alpha}+\hat{\beta}X_{i}\) can be calculated at the values \(X_{i}\) of the explanatory variable \(X\) for each unit \(i\) in the observed sample. These can then be compared to the correponding values \(Y_{i}\) of the response variable. Their differences \(Y_{i}-\hat{Y}_{i}\) are known as the (sample) residuals. These quantities are illustrated in Figure 8.9. This shows a fitted regression line, which is in fact the one for IMR given School enrolment also shown in Figure 8.6. Also shown are two points \((X_{i}, Y_{i})\). These are also from Figure 8.6; the rest have been omitted to simplify the plot. The point further to the left is the one for Mali, which has School enrolment \(X_{i}=43.0\) and IMR \(Y_{i}=14.1\). Using the estimated coefficients \(\hat{\alpha}=19.736\) and \(\hat{\beta}=-0.179\) in Figure 8.7, the fitted value for Mali is \(\hat{Y}_{i}=19.736-0.179\times 43.0=12.0\). Their difference is the residual \(Y_{i}-\hat{Y}_{i}=14.1-12.0=2.1\). Because the observed value is here larger than the fitted value, the residual is positive and the observed value is above the fitted line, as shown in Figure 8.9.

The second point shown in Figure 8.9 corresponds to the observation for Ghana, for which \(X_{i}=58.0\) and \(Y_{i}=5.7\). The fitted value is then \(\hat{Y}_{i}=19.736-0.179\times 58.0=9.4\) and the residual \(Y_{i}-\hat{Y}_{i}=5.7-9.4=-3.7\). Because the observed value is now smaller than the fitted value, the residual is negative and the observed \(Y_{i}\) is below the fitted regression line.

So far we have still not explained how the specific values of the parameter estimates in Figure 8.7 were obtained. In doing so, we are faced with the task of identifying a regression line which provides the best fit to the observed points in a scatterplot like Figure 8.6. Each possible choice of \(\hat{\alpha}\) and \(\hat{\beta}\) corresponds to a different regression line, and some choices are clearly better than others. For example, it seems intuitively obvious that it would be better for the line to go through the cloud of points rather than stay completely outside it. To make such considerations explicit, the residuals can be used as a criterion of model fit. The aim will then be to make the total magnitude of the residuals as small as possible, so that the fitted line is as close as possible to the observed points \(Y_{i}\) in some overall sense. This cannot be done simply by adding up the residuals, because they can have different signs, and positive and negative residuals could thus cancel out each other in the addition. As often before, the way around this is to remove the signs by considering the squares of the residuals. Summing these over all units \(i\) in the sample leads to the sum of squared residuals \[SSE = \sum (Y_{i}-\hat{Y}_{i})^{2}.\] Here \(SSE\) is short for Sum of Squares of Errors (it is also often called the Residual Sum of Squares or \(RSS\)). This is the quantity used as the criterion in estimating regression coefficients for a linear model. Different candidate values for \(\hat{\alpha}\) and \(\hat{\beta}\) lead to different values of \(\hat{Y}_{i}\) and thus of \(SSE\). The final estimates are the ones which give the smallest value of \(SSE\). Their formulas are \[\begin{equation} \hat{\beta}=\frac{\sum (X_{i}-\bar{X})(Y_{i}-\bar{Y})}{\sum (X_{i}-\bar{X})^{2}}=\frac{s_{xy}}{s_{x}^{2}} \tag{8.5} \end{equation}\] and \[\begin{equation} \hat{\alpha}=\bar{Y}-\hat{\beta}\bar{X} \tag{8.6} \end{equation}\] where \(\bar{Y}\), \(\bar{X}\), \(s_{x}\) and \(s_{xy}\) are the usual sample means, standard deviations and covariances for \(Y\) and \(X\). These are known as the least squares estimates of the regression coefficients (or as Ordinary Least Squares or OLS estimates), and the reasoning used to obtain them is the method of least squares.49 Least squares estimates are almost always used for linear regression models, and they are the ones displayed by SPSS and other software. For our model for IMR given School enrolment, the estimates are the \(\hat{\alpha}=19.736\) and \(\hat{\beta}=-0.179\) shown in Figure 8.7.

The estimated coefficients can be used to calculate predicted values for \(Y\) at any values of \(X\), not just those included in the observed sample. For instance, in the infant mortality example the predicted IMR for a country with School enrolment of 80% would be \(\hat{Y}=19.736-0.179\times 80=5.4\). Such predictions should usually be limited to the range of values of \(X\) actually observed in the data, and extrapolation beyond these values should be avoided.

The most common estimate of the remaining parameter of the model, the residual standard deviation \(\sigma\), is \[\begin{equation} \hat{\sigma}=\sqrt{\frac{\sum \left ( Y_{i}-\hat{Y}_{i}\right ) ^{2}}{n- \left ( k+1 \right )}}=\sqrt{\frac{SSE}{n- \left ( k+1 \right )}} \tag{8.7} \end{equation}\] where \(k\) is here set equal to 1. This bears an obvious resemblance to the formula for the basic sample standard deviation, shown for \(Y_{i}\) in ((8.1)). One difference to that formula is that the denominator of ((8.7)) is shown as \(n-(k+1)\) rather than \(n-1\). Here \(k=1\) is the number of explanatory variables in the model, and \(k+1=2\) is the number of regression coefficients (\(\alpha\) and \(\beta\)) including the constant term \(\alpha\). The quantity \(n-(k+1)\), i.e. here \(n-2\), is the degrees of freedom (\(df\)) of the parameter estimates. We will need it again in the next section. It is here given in the general form involving the symbol \(k\), so that we can later refer to the same formula for models with more explanatory variables and thus \(k\) greater than 1. In SPSS output, the degrees of freedom are shown in the “ANOVA” table under “df” for “Residual”. In the infant mortality example \(n=111\), \(k=1\) and \(df=111-2=109\), as shown in Figure 8.7.

Finally, two connections between previous topics and the parameters \(\hat{\alpha}\), \(\hat{\beta}\) and \(\hat{\sigma}\) are worth highlighting:

The estimated slope \(\hat{\beta}\) from ((8.5)) is related to the sample correlation \(r\) from ((8.3)) by \(r=(s_{x}/s_{y})\,\hat{\beta}\). In both of these it is \(\hat{\beta}\) which carries information about the association between \(X\) and \(Y\). The ratio \(s_{x}/s_{y}\) serves only to standardise the correlation coefficient so that it is always between \(-1\) and \(+1\). The slope coefficient \(\hat{\beta}\) is not standardised, and the interpretation of its magnitude depends on the units of measurement of \(X\) and \(Y\) in the way defined in Section 8.3.3.

Suppose we simplify the simple linear regression model ((8.4)) further by setting \(\beta=0\), thus removing \(\beta X\) from the model. The new model states that all \(Y_{i}\) are normally distributed with the same mean \(\alpha\) and standard deviation \(\sigma\). Apart from the purely notational difference of using \(\alpha\) instead of \(\mu\), this is exactly the single-sample model considered in Section 7.4. Using the methods of this section to obtain estimates of the two parameters of this model also leads to exactly the same results as before. The least squares estimate of \(\alpha\) is then \(\hat{\alpha}=\bar{Y}\), obtained by setting \(\hat{\beta}=0\) in ((8.6)). Since there is no \(\hat{\beta}\) in this case, \(\hat{Y}_{i}=\bar{Y}\) for all observations, \(k=0\) and \(df=n-(k+1)=n-1\). Substituting these into ((8.7)) shows that \(\hat{\sigma}\) is then equal to the usual sample standard deviation \(s_{y}\) of \(Y_{i}\).

Coefficient of determination (\(R^{2}\))

The coefficient of determination, more commonly known as \(\mathbf{R^{2}}\) (“R-squared”), is a measure of association very often used to describe the results of linear regression models. It is based on the same idea of sums of squared errors as least squares estimation, and on comparison of them between two models for \(Y\). The first of these models is the very simple one where the explanatory variable \(X\) is not included at all. As discussed above, the estimate of the expected value of \(Y\) is then the sample mean \(\bar{Y}\). This is the best prediction of \(Y\) we can make, if the same predicted value is to be used for all observations. The error in the prediction of each value \(Y_{i}\) in the observed data is then \(Y_{i}-\bar{Y}\) (c.f. Figure 8.9 for an illustration of this for one observation). The sum of squares of these errors is \(TSS=\sum (Y_{i}-\bar{Y})^{2}\), where \(TSS\) is short for “Total Sum of Squares”. This can also be regarded as a measure of the total variation in \(Y_{i}\) in the sample (note that \(TSS/(n-1)\) is the usual sample variance \(s^{2}_{y}\)).

When an explanatory variable \(X\) is included in the model, the predicted value for each \(Y_{i}\) is \(\hat{Y}_{i}=\hat{\alpha}+\hat{\beta}X_{i}\), the error in this prediction is \(Y_{i}-\hat{Y}_{i}\), and the error sum of squares is \(SSE=\sum (Y_{i}-\hat{Y}_{i})^{2}\). The two sums of squares are related by \[\begin{equation} \sum (Y_{i}-\bar{Y})^{2} =\sum (Y_{i}-\hat{Y}_{i})^{2} +\sum(\hat{Y}_{i}-\bar{Y})^{2}. \tag{8.8} \end{equation}\] Here \(SSM=\sum (\hat{Y}_{i}-\bar{Y})^{2}=TSS-SSE\) is the “Model sum of squares”. It is the reduction in squared prediction errors achieved when we make use of \(X_{i}\) to predict values of \(Y_{i}\) with the regression model, instead of predicting \(\bar{Y}\) for all observations. In slightly informal language, \(SSM\) is the part of the total variation \(TSS\) “explained” by the fitted regression model. In this language, ((8.8)) can be stated as

| Total variation of \(Y\) | = | Variation explained by regression | + | Unexplained variation |

| \(TSS\) | \(=\) | \(SSM\) | \(+\) | \(SSE\) |

The \(R^{2}\) statistic is defined as \[\begin{equation} R^{2}= \frac{TSS-SSE}{TSS} = 1-\frac{SSE}{TSS}=1-\frac{\sum (Y_{i}-\hat{Y}_{i})^{2}}{\sum (Y_{i}-\bar{Y})^{2}}. \tag{8.9} \end{equation}\] This is the proportion of the total variation of \(Y\) in the sample explained by the fitted regression model. Its smallest possible value is 0, which is obtained when \(\hat{\beta}=0\), so that \(X\) and \(Y\) are completely unassociated, \(X\) provides no help for predicting \(Y\), and thus \(SSE=TSS\). The largest possible value of \(R^{2}\) is 1, obtained when \(\hat{\sigma}=0\), so that the observed \(Y\) can be predicted perfectly from the corresponding \(X\) and thus \(SSE=0\). More generally, \(R^{2}\) is somewhere between 0 and 1, with large values indicating strong linear association between \(X\) and \(Y\).

\(R^{2}\) is clearly a Proportional Reduction of Error (PRE) measure of association of the kind discussed in Section 2.4.5, with \(E_{1}=TSS\) and \(E_{2}=SSE\) in the notation of equation for the PRE measure of association in Section 2.4.5. It is also related to the correlation coefficient. In simple linear regression, \(R^{2}\) is the square of the correlation \(r\) between \(X_{i}\) and \(Y_{i}\). Furthermore, the square root of \(R^{2}\) is the correlation between \(Y_{i}\) and the fitted values \(\hat{Y}_{i}\). This quantity, known as the multiple correlation coefficient and typically denoted \(R\), is always between 0 and 1. It is equal to the correlation \(r\) between \(X_{i}\) and \(Y_{i}\) when \(r\) is positive, and the absolute value (removing the \(-\) sign) of \(r\) when \(r\) is negative. For example, for our infant mortality model \(r=-0.753\), \(R^{2}=r^{2}=0.567\) and \(R=\sqrt{R^{2}}=0.753\).

In SPSS output, the “ANOVA” table shows the model, error and total sums of squares \(SSM\), \(SSE\) and \(TSS\) in the “Sum of Squares column”, on the “Regression”, “Residual” and “Total” rows respectively. \(R^{2}\) is shown in “Model summary” under “R Square” and multiple correlation \(R\) next to it as “R”. Figure 8.7 shows these results for the model for IMR given School enrolment. Here \(R^{2}=0.567\). Using each country’s level of school enrolment to predict its IMR thus reduces the prediction errors by 56.7% compared to the situation where the predicted IMR is the overall sample mean (here 4.34) for every country. Another conventional way of describing this \(R^{2}\) result is to say that the variation in rates of School enrolment explains 56.7% of the observed variation in Infant mortality rates.

\(R^{2}\) is a useful statistic with a convenient interpretation. However, its importance should not be exaggerated. \(R^{2}\) is rarely the only or the most important part of the model results. This may be the case if the regression model is fitted solely for the purpose of predicting future observations of the response variable. More often, however, we are at least or more interested in examining the nature and strength of the associations between the response variable and the explanatory variable (later, variables), in which case the regression coefficients are the main parameters of interest. This point is worth emphasising because in our experience many users of linear regression models tend to place far too much importance on \(R^{2}\), often hoping to treat it as the ultimate measure of the goodness of the model. We are frequently asked questions along the lines of “My model has \(R^{2}\) of 0.42 — is that good?”. The answer tends to be “I have no idea” or, at best, “It depends”. This not a sign of ignorance, because it really does depend:

Which values of \(R^{2}\) are large or small or “good” is not a statistical question but a substantive one, to which the answer depends on the nature of the variables under consideration. For example, most associations between variables in the social sciences involve much unexplained variation, so their \(R^{2}\) values tend to be smaller than for quantities in, say, physics. Similarly, even in social sciences models for aggregates such as countries often have higher values of \(R^{2}\) than ones for characteristics of individual people. For example, the \(R^{2}=0.567\) in our infant mortality example (let alone the \(R^{2}=0.753\) we will achieve for a multiple linear model for IMR in Section 8.6) would be unachievably high for many types of individual-level data.

In any case, achieving large \(R^{2}\) is usually not the ultimate criterion for selecting a model, and a model can be very useful without having a large \(R^{2}\). The \(R^{2}\) statistic reflects the magnitude of the variation around the fitted regression line, corresponding to the residual standard deviation \(\hat{\sigma}\). Because this is an accepted part of the model, \(R^{2}\) is not a measure of how well the model fits: we can have a model which is essentially true (in that \(X\) is linearly associated with \(Y\)) but has large residual standard error and thus small \(R^{2}\).

8.3.5 Statistical inference for the regression coefficients

The only parameter of the simple linear regression model for which we will describe methods of statistical inference is the slope coefficient \(\beta\). Tests and confidence intervals for population values of the intercept \(\alpha\) are rarely and ones about the residual standard deviation \(\sigma\) almost never substantively interesting, so they will not be considered. Similarly, the only null hypothesis on \(\beta\) discussed here is that its value is zero, i.e. \[\begin{equation} H_{0}:\; \beta=0. \tag{8.10} \end{equation}\] Recall that when \(\beta\) is 0, there is no linear association between the explanatory variable \(X\) and the response variable \(Y\). Graphically, this corresponds to a regression line in the population which is parallel to the \(X\)-axis (see plot (d) of Figure 8.4 for an illustration of such a line in a sample). The hypothesis ((8.10)) can thus be expressed in words as \[\begin{equation} H_{0}:\; \text{\emph{There is no linear association between }} X \text{\emph{and }} Y \text{ \emph{in the population}}. \tag{8.11} \end{equation}\] Tests of this are usually carried out against a two-sided alternative hypothesis \(H_{a}: \; \beta\ne 0\), and we will also concentrate on this case.

Formulation ((8.11)) implies that the hypothesis that \(\beta=0\) is equivalent to one that the population correlation \(\rho\) between \(X\) and \(Y\) is also 0. The test statistic presented below for testing ((8.10)) is also identical to a common test statistic for \(\rho=0\). A test of \(\beta=0\) can thus be interpreted also as a test of no correlation in the population.

The tests and confidence intervals involve both the estimate \(\hat{\beta}\) and its estimated standard error, which we will here denote \(\hat{\text{se}}(\hat{\beta})\).50 It is calculated as \[\begin{equation} \hat{\text{se}}(\hat{\beta})=\frac{\hat{\sigma}}{\sqrt{\sum\left(X_{i}-\bar{X}\right)^{2}}}=\frac{\hat{\sigma}}{s_{x}\sqrt{n-1}} \tag{8.12} \end{equation}\] where \(\hat{\sigma}\) is the estimated residual standard deviation given by ((8.7)), and \(s_{x}\) is the sample standard deviation of \(X\). The standard error indicates the level of precision with which \(\hat{\beta}\) estimates the population parameter \(\beta\). The last expression in ((8.12)) shows that the sample size \(n\) appears in the denominator of the standard error formula. This means that the standard error becomes smaller as the sample size increases. In other words, the precision of estimation increases when the sample size increases, as with all the other estimates of population parameters we have considered before. In SPSS output, the estimated standard error is given under “Std. Error” in the “Coefficients” table. Figure 8.7 shows that \(\hat{\text{se}}(\hat{\beta})=0.015\) for the estimated coefficient \(\hat{\beta}\) of School enrolment.

The test statistic for the null hypothesis ((8.10)) is once again of the general form (see the beginning of Section 5.5.2), i.e. a point estimate divided by its standard error. Here this gives \[\begin{equation} t=\frac{\hat{\beta}}{\hat{\text{se}}(\hat{\beta})}. \tag{8.13} \end{equation}\] The logic of this is the same as in previous applications of the same idea. Since the null hypothesis ((8.10)) claims that the population \(\beta\) is zero, values of its estimate \(\hat{\beta}\) far from zero will be treated as evidence against the null hypothesis. What counts as “far from zero” depends on how precisely \(\beta\) is estimated from the observed data by \(\hat{\beta}\) (i.e. how much uncertainty there is in \(\hat{\beta}\)), so \(\hat{\beta}\) is standardised by dividing by its standard error to obtain the test statistic.

When the null hypothesis ((8.10)) is true, the sampling distribution of the test statistic ((8.13)) is a \(t\) distribution with \(n-2\) degrees of freedom (i.e. \(n-(k+1)\) where \(k=1\) is the number of explanatory variables in the model). The \(P\)-value for the test against a two-sided alternative hypothesis \(\beta\ne 0\) is then the probability that a value from a \(t_{n-2}\) distribution is at least as far from zero as the value of the observed test statistic. As for the tests of one and two means discussed in Chapter 7, it would again be possible to consider a large-sample version of the test which relaxes the assumption that \(Y_{i}\) given \(X_{i}\) are normally distributed, and uses (thanks to the Central Limit Theorem again) the standard normal distribution to obtain the \(P\)-value. With linear regression models, however, the \(t\) distribution version of the test is usually used and included in standard computer output, so only it will be discussed here. The difference between \(P\)-values from the \(t_{n-2}\) and standard normal distributions is in any case minimal when the sample size is reasonably large (at least 30, say).

In the infant mortality example shown in Figure 8.7, the estimated coefficient of School enrolment is \(\hat{\beta}=-0.179\), and its estimated standard error is \(\hat{\text{se}}(\hat{\beta})=0.015\), so the test statistic is \[t=\frac{-0.179}{0.015}=-11.94\] (up to some rounding error). This is shown in the “t” column of the “Coefficients” table. The \(P\)-value, obtained from the \(t\) distribution with \(n-2=109\) degrees of freedom, is shown in the “Sig.” column. Here \(P<0.001\), so the null hypothesis is clearly rejected. The data thus provide very strong evidence that primary school enrolment is associated with infant mortality rate in the population.

In many analyses, rejecting the null hypothesis of no association will be entirely unsurprising. The question of interest is then not whether there is an association in the population, but how strong it is. This question is addressed with the point estimate \(\hat{\beta}\), combined with a confidence interval which reflects the level of uncertainty in \(\hat{\beta}\) as an estimate of the population parameter \(\beta\). A confidence interval for \(\beta\) with the confidence level \(1-\alpha\) is given by \[\begin{equation} \hat{\beta} \pm t_{\alpha/2}^{(n-2)} \, \hat{\text{se}}(\hat{\beta}) \tag{8.14} \end{equation}\] where the multiplier \(t_{\alpha/2}^{(n-2)}\) is obtained from the \(t_{n-2}\) distribution as in previous applications of \(t\)-based confidence intervals (c.f. the description in Section 7.3.4). For a 95% confidence interval (i.e. one with \(\alpha=0.05\)) in the infant mortality example, the multiplier is \(t_{0.025}^{(109)}=1.98\), and the endpoints of the interval are \[-0.179-1.98\times 0.015=-0.209 \text{and} -0.179+1.98\times 0.015=-0.149.\] These are also shown in the last two columns of the “Coefficients” table of SPSS output. In this example we are thus 95% confident that the expected change in IMR associated with an increase of one percentage point in School enrolment is a decrease of between 0.149 and 0.209 percentage points. If you are calculating this confidence interval by hand, it is (if the sample size is at least 30) again acceptable to use the multiplier 1.96 from the standard normal distribution instead of the \(t\)-based multiplier. Here this would give the confidence interval \((-0.208; -0.150)\).

It is often more convenient to interpret the slope coefficient in terms of larger or smaller increments in \(X\) than one unit. As noted earlier, a point estimate for the effect of this is obtained by multiplying \(\hat{\beta}\) by the appropriate constant. A confidence interval for it is calculated similarly, by multiplying the end points of an interval for \(\hat{\beta}\) by the same constant. For example, the estimated effect of a 10-unit increase in School enrolment is \(10\times \hat{\beta}=-1.79\), and a 95% confidence interval for this is \(10\times (-0.209; -0.149)=(-2.09; -1.49)\). In other words, we are 95% confident that the effect is a decrease of between 2.09 and 1.49 percentage points.

8.4 Interlude: Association and causality

Felix, qui potuit rerum cognoscere causas,

atque metus omnis et inexorabile fatum

subiecit pedibus strepitumque Acherontis avariBlessed is he whose mind had power to probe

The causes of things and trample underfoot

All terrors and inexorable fate

And the clamour of devouring Acheron(Publius Vergilius Maro: Georgica (37-30 BCE), 2.490-492;

translation by L. P. Wilkinson)

These verses from Virgil’s Georgics are the source of the LSE motto — “Rerum cognoscere causas”, or “To know the causes of things” — which you can see on the School’s coat of arms on the cover of this coursepack. As the choice of the motto suggests, questions on causes and effects are of great importance in social and all other sciences. Causal connections are the mechanisms through which we try to understand and predict what we observe in the world, and the most interesting and important research questions thus tend to involve claims about causes and effects.

We have already discussed several examples of statistical analyses of associations between variables. Association is not the same as causation, as two variables can be statistically associated without being in any way directly causally related. Finding an association is thus not sufficient for establishing a causal link. It is, however, necessary for such a claim: if two variables are not associated, they will not be causally connected either. This implies that examination of associations must be a part of any analysis aiming to obtain conclusions about causal effects.

Definition and analysis of causal effects are considered in more detail on the course MY400 and in much greater depth still on MY457. Here we will discuss only the following simplified empirical version of the question.51 Suppose we are considering two variables \(X\) and \(Y\), and suspect that \(X\) is a cause of \(Y\). To support such a claim, we must be able to show that the following three conditions are satisfied:

There is a statistical association between \(X\) and \(Y\).

An appropriate time order: \(X\) comes before \(Y\).

All alternative explanations for the association are ruled out.

The first two conditions are relatively straightforward, at least in principle. Statistical associations are examined using the kinds of techniques covered on this course, and decisions about whether or not there is an association are usually made largely with the help of statistical inference. Note also that making statistical associations one of the conditions implies that this empirical definition of causal effects is not limited to deterministic effects, where a particular value of \(X\) always leads to exactly the same value of \(Y\). Instead, we consider probabilistic causal effects, where changes in \(X\) make different values of \(Y\) more or less likely. This is clearly crucial in the social sciences, where hardly any effects are even close to deterministic.

The second condition is trivial in many cases where \(X\) must logically precede \(Y\) in time: for example, a person’s sex is clearly determined before his or her income at age 20. In other cases the order is less obvious: for example, if we consider the relationship between political attitudes and readership of different newspapers, it may not be clear whether attitude came before choice of paper of vice versa. Clarifying the time order in such cases requires careful research design, often involving measurements taken at several different times.

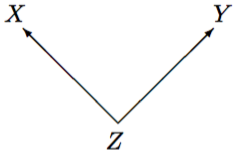

The really difficult condition is the third one. The list of “all alternative explanations” is essentially endless, and we can hardly ever be sure that all of them have been “ruled out”. Most of the effort and ingenuity in research design and analysis in a study of any causal hypothesis usually goes into finding reasonably convincing ways of eliminating even the most important alternative explanations. Here we will discuss only one general class of such explanations, that of spurious associations due to common causes of \(X\) and \(Y\). Suppose that we observe an association, here denoted symbolically by \(X\) — \(Y\), and would like to claim that this implies a causal connection \(X\longrightarrow Y\). One situation where such a claim is not justified is when both \(X\) and \(Y\) are caused by a third variable \(Z\), as in the graph in Figure 8.10. If we here consider only \(X\) and \(Y\), they will appear to be associated, but the connection is not a causal one. Instead, it is a spurious association induced by the dependence on both variables on the common cause \(Z\).

To illustrate a spurious association with a silly but memorable teaching example, suppose that we examine a sample of house fires in London, and record the number of fire engines sent to each incident (\(X\)) and the amount of damage caused by the fire (\(Y\)). There will be a strong association between \(X\) and \(Y\), with large numbers of fire engines associated with large amounts of damage. It is also reasonably clear that the number of fire engines is determined before the final extent of damage. The first two conditions discussed above are thus satisfied. We would, however, be unlikely to infer from this that the relationship is causal and conclude that we should try to reduce the cost of fires by dispatching fewer fire engines to them. This is because the association between the number of fire engines and the amount of damages is due to both of them being influenced by the size of the fire (\(Z\)). Here this is of course obvious, but in most real research questions possible spurious associations are less easy to spot.

How can we then rule out spurious associations due to some background variables \(Z\)? The usual approach is to try to remove the association between \(X\) and \(Z\). This means in effect setting up comparisons between units which have different values of \(X\) but the same or similar values of \(Z\). Any differences in \(Y\) can then more confidently be attributed to \(X\), because they cannot be due to differences in \(Z\). This approach is known as controlling for other variables \(Z\) in examining the association between \(X\) and \(Y\).

The most powerful way of controlling for background variables is to conduct a randomized experiment, where the values of the explanatory variable \(X\) can be set by the researcher, and are assigned at random to the units in the study. For instance, of the examples considered in Chapters 5 and 7, Examples 5.3, 5.4 and 7.3 are randomized experiments, each with an intervention variable \(X\) with two possible values (placebo or real vaccine, one of two forms of a survey question, and police officer wearing or not wearing sunglasses, respectively). The randomization assures that units with different values of \(X\) are on average similar in all variables \(Z\) which precede \(X\) and \(Y\), thus ruling out the possibility of spurious associations due to such variables.